June 24/July 1, 2019: Volume 35, Issue 1

By Megan Salzano

For the ninth consecutive year since the fallout of the Great Recession, the U.S. ceramic tile market registered growth. However, the growth witnessed in 2018 was not on par with the 5%-6% increase the category experienced in both volume and sales since 2016. In fact, many industry observers noted a significant slowdown in 2018.

For the ninth consecutive year since the fallout of the Great Recession, the U.S. ceramic tile market registered growth. However, the growth witnessed in 2018 was not on par with the 5%-6% increase the category experienced in both volume and sales since 2016. In fact, many industry observers noted a significant slowdown in 2018.

“In the past year, we saw growth in both residential and commercial segments for ceramic tile,” said Raj Shah, president, MSI International. “That said, the growth was the lowest we have seen since the economic crisis.”

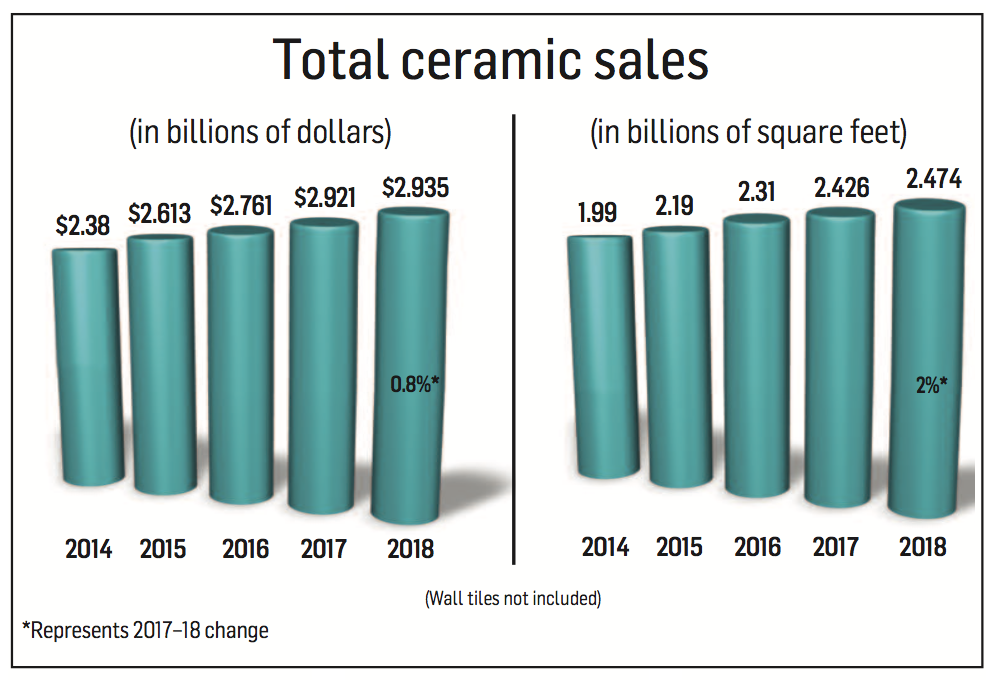

FCNews research shows the category saw about 2% growth in volume from 2.426 billion square feet in 2017 to 2.474 billion square feet in 2018. Sales were relatively flat for the category, registering less than 1% growth from $2.921 billion in 2017 to $2.935 billion last year. “It is important to note there was a lot of buildup of inventory, especially from China, during last quarter of 2018 in anticipation of higher tariffs scheduled to start January 1, 2019,” Gianni Mattioli, executive vice president of Dal-Tile, explained.

Even with the slowdown, the category still held strong in 2018 as the third-largest sector in flooring in terms of dollars and volume, representing 12.8% of all flooring sold in 2018—although down from 13.3% in 2017—and 12.6% of total industry volume, slightly up from 12.35% in 2017. Only the carpet/rugs and resilient categories accounted for more volume and sales.

Commercial gains

The commercial market saw a slightly better outcome in terms of growth when compared to residential. Commercial projects and spending continued on the growth path they have experienced since 2015. FCNews research showed ceramic’s share of the commercial market increased slightly to 15.4% last year, up from 14.1% in 2017. This was driven by strong growth in the hospitality, corporate, retail and assisted-living segments. Multi-family construction also rose in 2018.

Tile suppliers noted the ongoing success of wall tile within the commercial market and the possibility of its future growth within both the commercial and residential segments. “We have seen a renaissance in wall tile happen with all kinds of new formats and aesthetics being popularized in the market,” Shah said. “Long term, I believe the percentage of wall tile to floor tile will continue to grow as wall tile is not as susceptible to product substitution and due to the innovation in formats and aesthetics.”

Imports vs. domestic

U.S. imports in 2018 comprised about 70% of tile consumption in square feet, up from about 68% in 2017. In 2018, the U.S. imported 2.2 billion square feet of ceramic tile, up 4.7% from 2.1 billion square feet in 2017, according to the U.S. Department of Commerce.

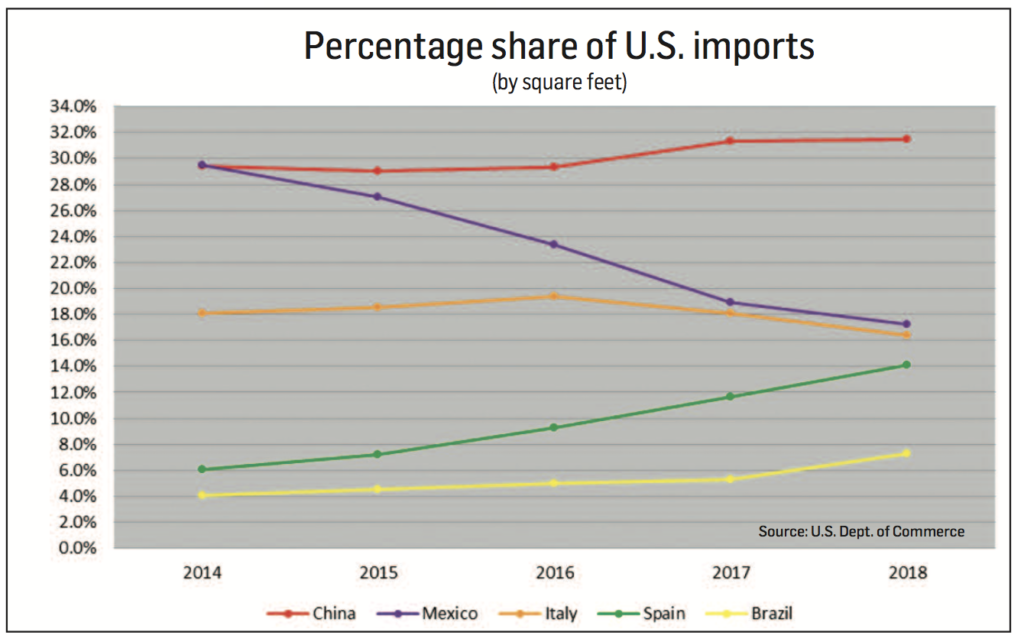

China remained the largest exporter of ceramic tile to the U.S. (in square feet), a position it has held each year since 2015. Chinese imports made up 31.5% of U.S. imports in 2018, the highest annual percentage China has ever held of the U.S. import market. The 10% tariff increase on Chinese ceramic tile imports imposed by the Trump administration took effect at the end of September but, according to the Tile Council of North America (TCNA), was unlikely to have a meaningful impact on China’s market position.

China remained the largest exporter of ceramic tile to the U.S. (in square feet), a position it has held each year since 2015. Chinese imports made up 31.5% of U.S. imports in 2018, the highest annual percentage China has ever held of the U.S. import market. The 10% tariff increase on Chinese ceramic tile imports imposed by the Trump administration took effect at the end of September but, according to the Tile Council of North America (TCNA), was unlikely to have a meaningful impact on China’s market position.

Despite the peso’s significant decline vs. the U.S. dollar over the last six years, losing nearly half its value, Mexican ceramic tile exports to the U.S. have fallen each year since 2015, the TCNA reported. In 2018, tile from Mexico comprised 17.3% of U.S. imports vs. 18.9% the year prior, the lowest share since 2006. Italy was the third-largest exporter of tile to the U.S. in 2018, making up 16.4% of U.S. imports, down from 18.1% in 2017. The next largest exporters to the U.S. were Spain (14.1%) and Brazil (7.3%).

In terms of dollars (including duty, freight and insurance), Italy remained the largest exporter to the U.S. in 2018, comprising 30.9% of U.S. imports. China was second with 27.3% and Spain was third with 15.6%.

Compared to 2017, U.S. shipments of ceramic tile in 2018 were down 5.4% to 911 million square feet. This marked the first year-over-year decline in domestic shipments since 2009. Even still, domestically produced tile is still the tile of choice for consumers as it accounted for 29.3% of all U.S. tile consumption in square feet in 2018. The next highest countries of origin were China (22.3%), Mexico (12.2%) and Italy (11.6%).

In dollar value, 2018 U.S. FOB factory sales of domestic shipments were down 4.4% to $1.39 billion, vs. $1.45 billion in 2017. (FOB port means the seller pays for transportation of the goods to the port of shipment, plus loading costs. The buyer pays the cost of marine freight transport, insurance, unloading and transportation from the arrival port to the final destination.) Domestically produced tile comprised 37.7% of total U.S. tile consumption by dollar value. The per-unit value of domestic shipments increased from $1.51 in 2017 to $1.53 in 2018.

U.S. ceramic tile exports in 2018 were 29.7 million square feet, up 4.4% vs. 2017. Most of these exports were to Canada (79.6%) and Mexico (4.5%).

Ongoing challenges

Industry observers cite several challenges that led to the reduced tile consumption in 2018. Among them: tariff wars, a less robust housing market, competition from other categories and continuing labor/installation woes. “Generally speaking, it was a strong economy throughout the year,” MSI’s Shah said. “That said, beginning in the second quarter a lot of confidence began to deteriorate with the threat of trade wars between China and the U.S. Section 301 tariffs did get set at 10% with a threat of 25% for most of the year, which hurt overall confidence. The third and fourth quarters of 2018 were dramatically slower than the first half of 2019 for ceramic tile.”

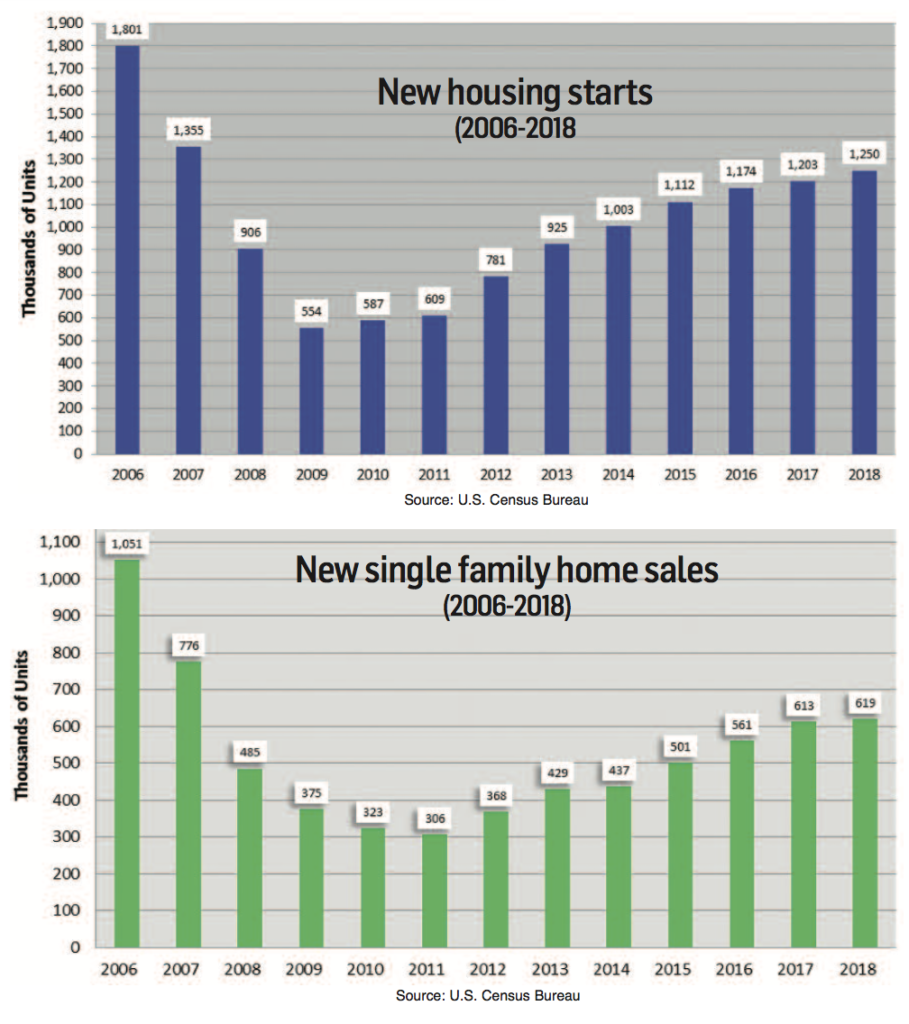

One key indicator for the health of ceramic tile is that of the housing market, which continued to have heavy implications for 2018. “After the end of the recession, the ceramic tile market increased quite a bit, but last year the increase became very small compared to previous years,” said Donato Grosser, industry consultant. “The main reason is the housing market is not moving—it’s basically flat. Housing is a very important factor for ceramic tile. During the recession housing starts fell by more than 70%, tile declined 30% and you saw that immediate decline.”

Grosser added that while the remodeling segment of the housing market is doing fairly well, “we don’t sell as much tile in remodeling projects as we do with new projects.”

Grosser added that while the remodeling segment of the housing market is doing fairly well, “we don’t sell as much tile in remodeling projects as we do with new projects.”

Competition from other categories, namely resilient, also put pressure on tile. “LVT is widely reported to have been the largest growth category in flooring in 2018, taking significant share and putting pressure on other categories of flooring,” said Jeff Daniel, vice president of sales support and planning, Emser Tile.

The novelty and low cost of LVT—and its WPC/SPC brethren—were major factors for its growth, observers said. “It’s a new product, it’s inexpensive, it’s easy to install and people are not looking at which product is superior; they’re looking at how much they’re spending,” Grosser explained. “People look at the first thing— cost. Then, the second—looks. That’s basically what affects the whole market and part of ceramic tile.”

In order to push back against LVT, suppliers said continued innovation within the category as well as adding value will be key. Some also noted several advantages tile already has in the market that should be better leveraged. For example, MSI’s Shah noted the growing popularity of new looks in tile vs. current LVT visuals. “LVT is still primarily a wood-look category,” he explained. “We are starting to see more non-wood visuals coming to market. The aesthetics available in ceramic tile that are non-wood still are significantly higher quality than can be found in LVT. In addition, with LVT there are technical difficulties with certain looks that are available in ceramic tile. This remains an opportunity for the LVT market, but at the same time it seems ceramic tile has a large head start in these looks.”

Emser’s Daniel focused on the upside—the belief that ceramic tile has not been as heavily impacted as other flooring categories by LVT’s growth. “Based on our view that the tile category continued to grow year over year, the market share pressure was likely hardest felt in soft flooring and wood categories.”

Another challenge the category continues to struggle with is the shortage of qualified installers. “This problem continued to be present in 2018,” Shah said. “This definitely accelerated the push toward LVT, which has a faster and lower install cost.”

Emser’s Daniel agreed, adding: “It is certainly impacting the cost of the final delivered product to the owner/buyer of both residential and nonresidential builds. There are issues with delays due to labor, but most issues appear to be pressures on the installation cost side due to competition for qualified labor. Innovation in products that require less labor to install will help offset labor time and cost.”

Looking ahead

While the ceramic tile market slowed its growth in 2018, sup- pliers are hopeful about the category’s potential for the remainder of this year and into 2020. “Innovation will continue to be the key to growth in the future,” Dal-Tile’s Mattioli said. “Advancements in decoration technology and impressive sizes such as 5 x 10-foot porcelain slabs are examples of how tile has been an innovation leader in the flooring industry.”

Pre-recession numbers remain on the minds of industry observers. For the category to return to its heyday, some believe both commercial and residential construction will have to continue on the path of stable growth. “Despite the long post-recession recovery, many would argue we are still falling 10%-15% short of the annual residential starts number to support population and demographics,” Daniel noted. “Affordability aside, that supply shortage would aid to the growth in the category when realized.”

Overall, ceramic tile has its inherent qualities that keep end users—both big and small—coming back for more. MSI’s Shah noted that ceramic tile continues to be the flooring option that has the highest longevity, least maintenance and most décor options.

“As an industry we can continue to see growth in ceramic by making it affordable and accessible,” he explained. “This specifically means making sure there is inherent value in all of the positive aspects ceramic tile has to offer while bringing more innovative aesthetics and performance that consumers are looking. At the same time, we have to take into account the relative value and competing products.”