June 26-July 2, 2018: Volume 34, Issue 1

By Lindsay Baillie

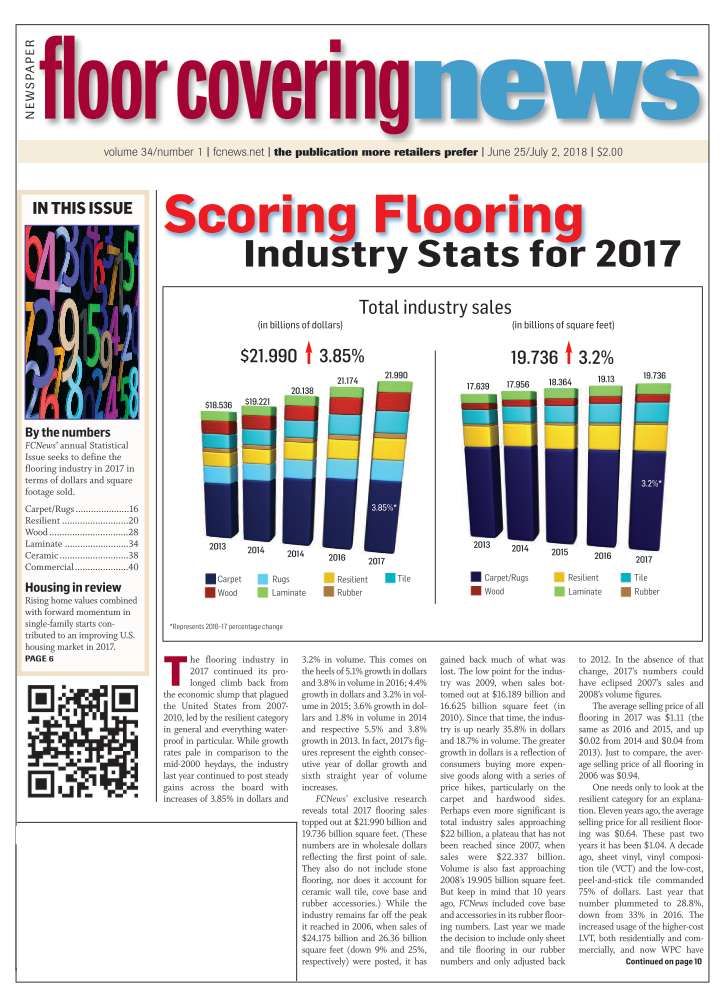

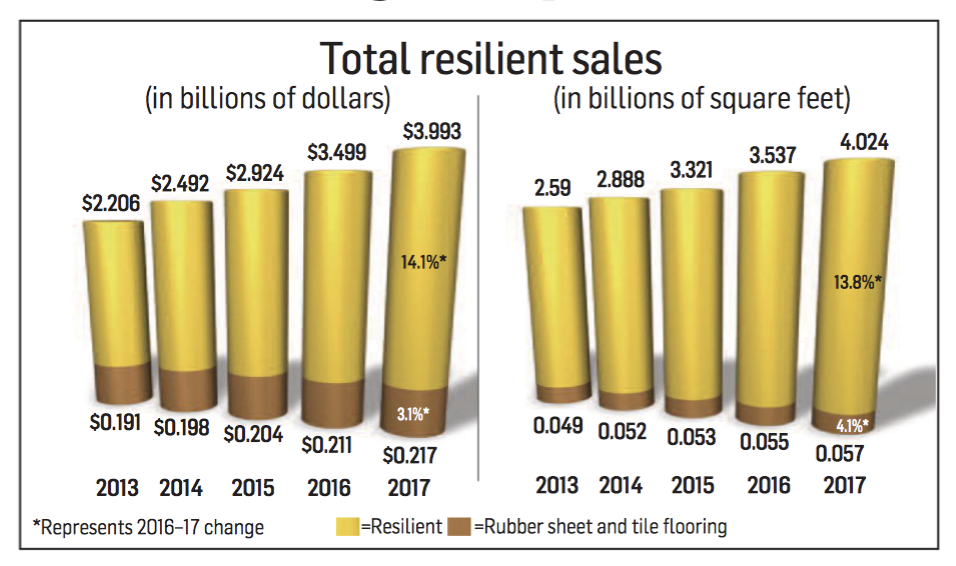

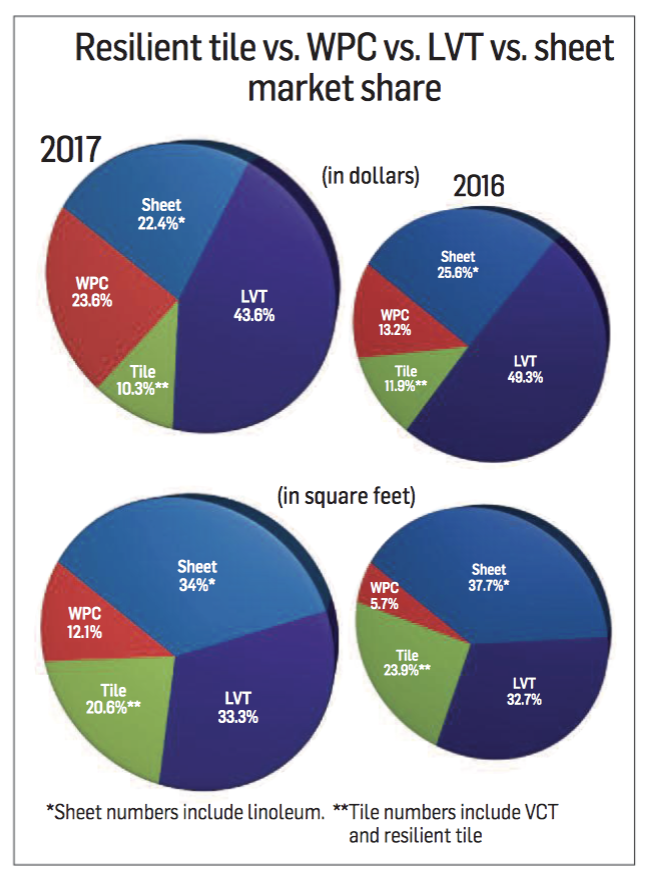

The resilient category once again led the flooring industry in terms of percentage growth, thanks mainly to the performance of sub-categories such as WPC and SPC. FCNews research shows the category generated $3.993 billion in sales in 2017—an industry-leading 14.1% increase over 2016’s $3.499 billion. In terms of volume, the category racked in 4.024 billion square feet at the first point of sales, a 13.8% increase from 2016’s 3.537 billion square feet.

The resilient category once again led the flooring industry in terms of percentage growth, thanks mainly to the performance of sub-categories such as WPC and SPC. FCNews research shows the category generated $3.993 billion in sales in 2017—an industry-leading 14.1% increase over 2016’s $3.499 billion. In terms of volume, the category racked in 4.024 billion square feet at the first point of sales, a 13.8% increase from 2016’s 3.537 billion square feet.

The resilient sector’s chart-busting performance in 2017 comes even more into focus when measured against other hard surfaces. When stacked up against ceramic tile, hardwood, laminate and other hard surface materials, resilient accounted for 30.34% of sales. When taking total flooring sales into account, resilient represented 18.15% of revenue and 20.4% of volume.

What’s even more impressive is the fact that resilient flooring’s percentage increase in revenue is a little over three-and-a-half times the growth of the entire industry, while volume growth is approximately five times that of the flooring sector as a whole.

Resilient’s double-digit growth in sales in 2017 is even more significant when looking at its performance over the past few years. FCNews research shows 2017’s sales represent a 36.6% increase over 2015’s $2.924 billion and a 60.2% increase com- pared to 2014. To put resilient’s growth into perspective, total resilient sales increased by 96.2% from 2012’s $2.035 and 81.8% from 2007. Meanwhile, total resilient volume increased 65.6% from 2012’s 2.43 billion square feet and 23.8% increase over 2007. The greater percent of increase from 2012 compared to 2007, observers say, reflects the effects of the Great Recession, which had just started in 2007 but was felt through 2012.

Industry executives cite several factors that contributed to another year of stellar growth of the category. One of which is the lingering effects of an improving economy. As Kurt Denman, chief marketing officer and executive vice president, sales, Congoleum, explained, “Fundamentally, the economy is good. Consumer confidence is high and there’s a ton of building going on, which has helped in all aspects of resilient.”

Many resilient manufacturers also point to the overwhelming success of WPC and rigid core products. “Multi-layer flooring is leading the way in LVT growth,” said Russ Rogg, president and CEO, Metroflor Corp. “While other variations are also growing, multi-layer flooring is outpacing glue-down and other varieties in a significant way.”

Executives like David Sheehan, senior vice president, product management, Mohawk Industries, believe WPC and rigid core continue to help push the resilient needle as more people discover the products’ benefits. “Floors that are rigid in nature are the darlings of the industry and have captured the attention of many sales associates and, in some cases, are being oversold to customers,” he noted.

Another key factor driving resilient sales is the constant innovation surrounding LVT, WPC and rigid core products. “Compared to other flooring categories, the LVT sector has seen many changes from additional looks, durability, availability and sheer innovation,” Jamey Block, vice president, product management resilient, Armstrong Flooring, told FCNews.

Another key factor driving resilient sales is the constant innovation surrounding LVT, WPC and rigid core products. “Compared to other flooring categories, the LVT sector has seen many changes from additional looks, durability, availability and sheer innovation,” Jamey Block, vice president, product management resilient, Armstrong Flooring, told FCNews.

Beyond the category’s various product attributes, another driving factor is the number of manufacturers in the resilient game. “More people are discovering the benefits of resilient flooring,” said Steven Ehrlich, vice president of sales and marketing, Novalis Innovative Flooring. “That discovery fuels demand, which, in turn, fuels more production—and so on.” Another factor is the growing availability of resilient across a variety of flooring brands, he added.

Residential rules the roost

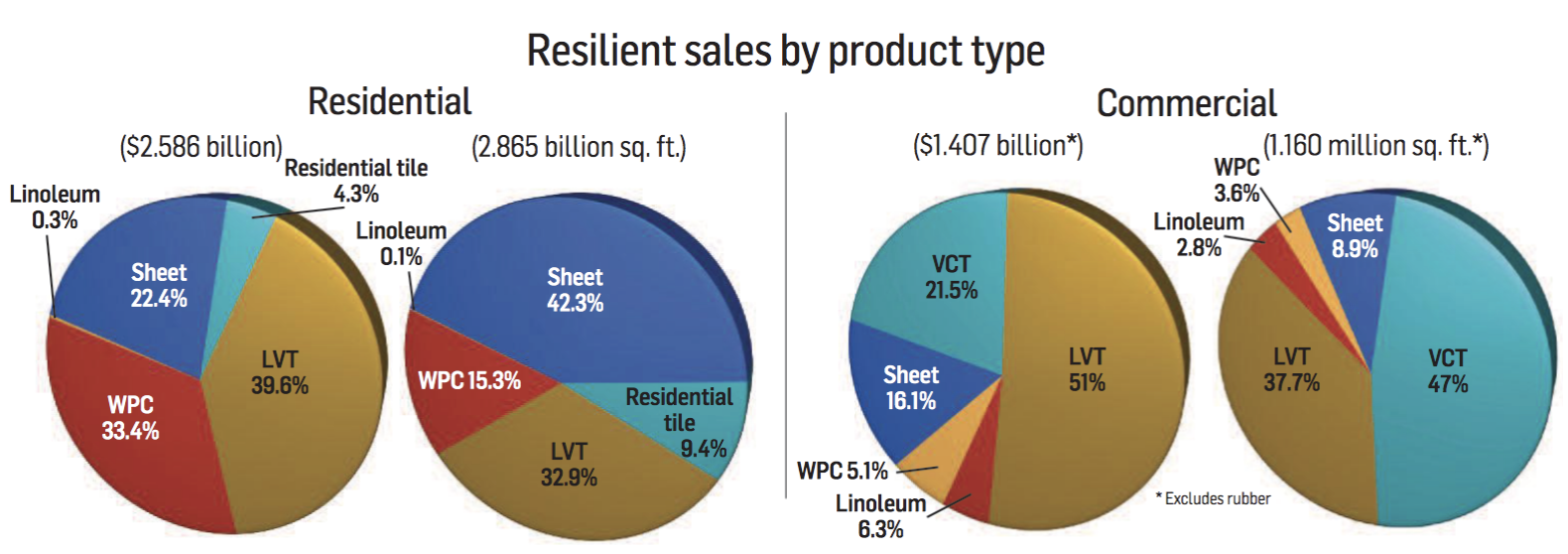

FCNews research shows the residential market made up almost 64.76% of total resilient revenue or $2.586 billion. Residential resilient also accounted for nearly 71.8% of total resilient volume. What’s more, residential LVT (including WPC and SPC) finished out 2017 with an estimated $1.888 billion in revenue, representing 73% of total residential resilient sales. In terms of square feet, research shows this red-hot product garnered 1.379 billion square feet, or 48.1%, of residential resilient volume.

Resilient manufacturers attribute the category’s stellar performance, in part, to the strength of key end-use sectors. While some industry executives see the greatest activity in the replacement/redesign markets, others are finding their products being used in builder/new home construction applications—including both single- and multi- family installations. However, most executives agree each segment is seeing a different resilient product take over market share.

For Armstrong, the replacement market continues to be strong. “We’re seeing strong growth across channels for remodel work,” Block explained. “We are also seeing a lot of excitement in new home construction with [rigid] products.”

According to David Kim, managing partner, NuFlors, single- and multi-family in new home as well as residential remodel saw improved growth in 2017. “Both [sectors] are expected to surge as the year continues,” he said. “As new construction has seen continued growth the last 10 years, we also see replacement growth as new technologies make it easier to replace and renovate existing floors.”

According to David Kim, managing partner, NuFlors, single- and multi-family in new home as well as residential remodel saw improved growth in 2017. “Both [sectors] are expected to surge as the year continues,” he said. “As new construction has seen continued growth the last 10 years, we also see replacement growth as new technologies make it easier to replace and renovate existing floors.”

While some manufacturers are seeing mostly WPC and rigid in the multi-family segment, other companies feel more dry- back is being installed. “That’s where the majority of the dryback business is,” Lindsey Nisbet, marketing director, EarthWerks, told FCNews. “[Builder] may be taken over by WPC, but [dryback] is standing strong in multi-family.”

Within residential LVT, click, floating and dryback products saw quite the shakeup. Back in 2016, click represented 39.7% of LVT revenue. In 2017 that number jumped to 55.1%. The large increase in click sales, observers say, resulted in a percent decrease for both floating and dryback products, which went from 6.8% to 4.8% and 53.5% to 40.3%, respectively.

Last year proved to be a big year for WPC and SPC, which claimed 45.8% of residential LVT dollars. In terms of volume, the sector’s go-to products captured 31.8% of residential LVT. Despite click LVT’s growth in 2017, many are seeing the product lose share to WPC and SPC.

“Whether it’s WPC or rigid core, there are a couple of things they just do better,” Congoleum’s Denman said. “One is it’s an easier installation product because you’re not trying to get that floppy click to come together. It inherently has a stronger locking joint. Most of it is sold with a backing on it so you’re getting sound mitigation. Generally speaking, it’s a better perceived value. If you hand someone a floppy click product and a WPC product and tell them price is relatively the same, as a consumer you’d take the thicker one. Plus, they’re doing great things with it, such as embossed in register, enhanced edges, longer boards.”

Another factor in WPC and SPCs’ takeover is the decrease in click innovation, according to EarthWerks’ Nisbet. “We have some of our click products that are still doing well, but you don’t see a ton of new click products being developed. The rigidity of WPC and SPC products just make it easier to install and a higher performing product.”

While WPC has continued to steal market share from sheet and traditional LVT, it is now facing its own pressure from SPC. Most flooring executives see a place in the market for both WPC and SPC, citing their differentiating factors as being enough to keep both alive.

“We have been educating our salesforce along with the RSA and consumer as to the benefits of both WPC and SPC,” said Jamann Stepp, director ofmarketing and product management, USFloors. “It’s not that one is necessarily better than the other, but rather WPC is designed and geared toward residential installations while SPC is engineered for more of a commercial application. The growth of WPC/SPC will continue to affect the growth opportunities for sheet and flexible vinyl. However, there will continue to be a market for these producing traditional click LVT, but we are firm believers that WPC will continue to represent the majority of multi-layer flooring category sales,” Metroflor’s Rogg said. “WPC products, which generally have a more traditional LVT decorative surface, still offer benefits SPC products don’t—such as more authentic textures, lighter and more easily handled larger sizes and formats, better acoustic advantages and so forth.”

“We have been educating our salesforce along with the RSA and consumer as to the benefits of both WPC and SPC,” said Jamann Stepp, director ofmarketing and product management, USFloors. “It’s not that one is necessarily better than the other, but rather WPC is designed and geared toward residential installations while SPC is engineered for more of a commercial application. The growth of WPC/SPC will continue to affect the growth opportunities for sheet and flexible vinyl. However, there will continue to be a market for these producing traditional click LVT, but we are firm believers that WPC will continue to represent the majority of multi-layer flooring category sales,” Metroflor’s Rogg said. “WPC products, which generally have a more traditional LVT decorative surface, still offer benefits SPC products don’t—such as more authentic textures, lighter and more easily handled larger sizes and formats, better acoustic advantages and so forth.”

Sheet cedes share

As a result of LVT, WPC and SPCs’ continued success, sheet vinyl products continue to lose market share. According to FCNews research, the segment was down 2.8% from $596.1 mil- lion in 2016 to $579 million in 2017. What’s more, the category saw a 4.2% drop in volume.

In addition to the increased consumption of LVT and WPC, there are other factors affecting sheet’s market share, industry experts say. “Installation is a significant issue for all flooring, especially with sheet,” Mary Katherine Dyczko-Riglin, product manager of residential sheet vinyl, Mannington, explained. “It’s hard to find installers across the country. With the installation being perceived as easier for click products, that’s definitely helping it steal share. Things that have always traditionally been sheet are also seeing dryback start to come in and take its place.”

Heavy promotion of LVT and WPC is also a factor. “I think the numbers we’re seeing right now are indicative of people becoming very aggressive with overselling the capabilities of a low-end LVT,” said Michael Finelli, director, Beauflor USA.

Despite sheet’s continuous loss of market share to LVT and WPC products, most manufacturers don’t see the sub-segment going away for good. “There are certain price points that sheet goods will always be able to participate in that I don’t believe LVT or WPC will be able to,” said Drew Hash, vice president hard surface product category manager, Shaw Floors. “There’s a place for all of them—it just may not be the same mix that we see today.”

Mohawk also sees a place for sheet. “We’re convinced there’s always going to be a flexible market,” Sheehan said. “And the value proposition of sheet is still great.”

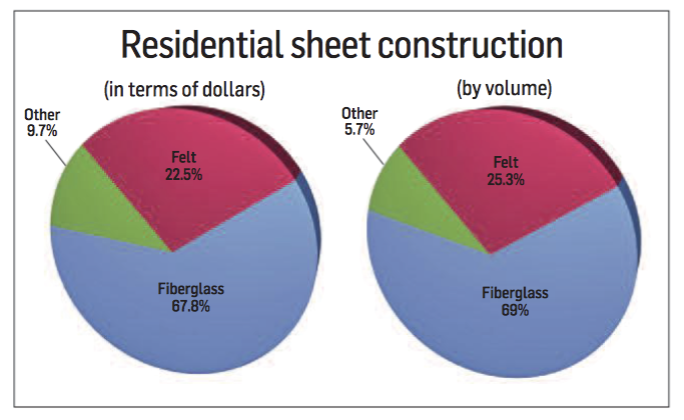

Within sheet, FCNewsresearch shows felt continues to lose market share to fiberglass. While felt was approximately 26.3% of sheet dollars and 29.7% of sheet volume in 2016, the product has dropped to 22.5% of dollars and 25.3% volume in 2017. Most manufacturers note the benefits of fiberglass as the products main selling point; however, many are still seeing success with felt.

“Felt is definitely continuing to lose share quicker than fiberglass,” Mannington’s Dyczko- Riglin said. “And it’s starting to lose share not only to fiberglass but to LVT. The fiberglass-backed products are typically a bit more installation friendly; they’re a bit more resilient to minor errors, handling issues, etc. They’re not going to break or permanently crease. Whereas with felt, you have to have a little more finesse.”

In addition to ease of installation, proponents say fiberglass-backed products offer comfort underfoot and water resistance. “While we do forecast the shift from felt to fiberglass to continue, Armstrong Flooring continues to bring industry-leading designs to our felt structures because we know there are still segments of the market and consumers that want a felt product,” Brock stated.

Congoleum is also seeing strength in its felt business. However, as Denman reports, the company is seeing some shifts in residential remodel, which is moving more toward LVT.

Some manufacturers believe the industry has only scratched the surface with respect to resilient’s global popularity and innovation. “LVT is still in an early growth stage,” said Jenne Ross, director of marketing, Karndean Designflooring. “We’re getting a lot of people who are still early adopters and are just finding out about the overall durability and performance of the product.”

Some manufacturers believe the industry has only scratched the surface with respect to resilient’s global popularity and innovation. “LVT is still in an early growth stage,” said Jenne Ross, director of marketing, Karndean Designflooring. “We’re getting a lot of people who are still early adopters and are just finding out about the overall durability and performance of the product.”

Commercial keeps climbing

Resilient products in the commercial space clocked in at $1.624 billion in 2017, a 28.5% increase from 2016, according to FCNews research. What’s more, the segment also saw a 17% increase in volume. Industry experts believe healthcare, education, Main Street and hospitality markets helped propel commercial growth. Experts also cite factors including the increased presence of WPC and rigid core products, and hard surface’s continued seizure of market share over soft surfaces.

“We’re seeing that kind of growth in every channel we service, whether that’s Main Street or traditional commercial,” Shaw’s Hash said. “I think that’s because the product offers just so many great attributes in every channel.”

Much of commercial’s sales came from commercial-grade LVT, which clocked in $796.5 million in 2017—a 22.8% growth over 2016’s $648.6 million. Within this sub-category, WPC made up a good portion of dollar growth, swelling from $24 million in 2016 to a little under $72 million in 2017. Dryback saw a 5.1% growth in volume, while click has started to see a drop-off—likely due to WPC’s growth in volume from 11.5 million square feet in 2016 to 41.7 million square feet in 2017.

“The movement from soft surface to hard surface is continuing to work its way into all commercial segments and is one of the contributing factors to resilient growth overall,” Armstrong’s Block explained. “The products’ looks as well as the demand for durability and ease of maintenance continue to propel resilient flooring solutions to the forefront.”

Michael Raskin, founder and CEO, Raskin Industries, has seen growth in hospitality in particular. Reason being? “Hotels are doing away with carpet because of poor maintenance, staining and odors. The benefits of LVT that apply to hospitality include durability, warm visuals and easy maintenance. In addition, we are offering acoustical backing to meet sound requirements.”

Al Boulogne, vice president, commercial resilient business, Mannington Commercial, sees traditional glue-down as the main driver of growth in specified contract applications. “While WPC and SPC have been huge drivers of growth on the residential side, it’s a little different on the commercial side,” he explained. “Even though WPC and SPC are certainly driving growth in multi-family and hospitality, for the more traditional commercial segments I still think it’s traditional LVT that is gaining momentum. There is so much about the category that pulls it through.”

Commercial sheet rose to approximately $224 million in 2017, a 4.9% uptick increase over 2016’s $213.5 million. This increase, according to resilient experts, is a result of multiple factors—not the least of which is product performance. “No doubt the increase in sheet is due to new products and advances in technologies,” said Jeff Collum, president and CEO, Shannon Specialty Floors. “We are also seeing an increase in sheet use in education, hospitality and government markets. Non-vinyl sheet is also capturing more and more commercial business.”

Commercial sheet rose to approximately $224 million in 2017, a 4.9% uptick increase over 2016’s $213.5 million. This increase, according to resilient experts, is a result of multiple factors—not the least of which is product performance. “No doubt the increase in sheet is due to new products and advances in technologies,” said Jeff Collum, president and CEO, Shannon Specialty Floors. “We are also seeing an increase in sheet use in education, hospitality and government markets. Non-vinyl sheet is also capturing more and more commercial business.”

VCT holds on

With all the talk surrounding commercial-grade LVT, WPC and the like, it’s easy to overlook traditional product categories such as vinyl composition tile (VCT). But statistics show the sub-category is still very much relevant. According to FCNews research, VCT saw a 0.6% increase in dollars (essentially flat) but a 7.7% increase in units.

“VCT provides unique value and long-term durability that high-traffic commercial customers appreciate and very few other products can replicate,” Armstrong Flooring’s Block said. (Armstrong Flooring purchased Mannington’s VCT business in 2017.) “We have also identified opportunity to further enhance this value with the extension of our Diamond 10 technology to the VCT category.”

Rubber rises up

FCNews research shows rubber generated $217 million in sales in 2017, a 3.1% uptick over 2016. In terms of volume, the category accounted for 57 million square feet, which translates to a 4.1% increase from last year. Some flooring executives attribute this overall increase to rubber’s use in areas other than heavy commercial environments. Others suggest rubber’s natural resiliency, resistance to stains, mildew and mold, and call for less chemicals makes it more appealing in places such as healthcare, hospitality and offices.

“As environmental concerns rise, specifiers are realizing rubber flooring’s green benefits,” said Joe Visintin, product manager, Tarkett North America. “For example, with no finish application required, fewer chemicals are required to maintain the floor and less water is used.”

Proponents believe rubber is receiving more attention thanks in part to updated visuals and innovative locking systems. Visintin sees rubber making its way from airports and schools to other areas as well such as healthcare waiting rooms, corporate hallways and offices, and hospitality lobbies.

Mike Tierney, national sales manager, Roppe, sees newer and brighter visuals as a driver for success. “Rubber flooring has always been popular in healthcare and education segments largely due to inherent traits such as the natural resiliency, resistance to stains, mildew and mold, comfort underfoot along with ease of maintenance,” he said. “However, newer colorations and versatile sizes or profile patterns make rubber flooring a great option for retail and hospitality spaces as well.”

Linoleum also shines

FCNews research shows linoleum experienced an 8.75% increase to $87 million from 2016’s $80 million. What’s more, its volume increased 8% to 32.25 million square feet. According to Denny Darragh, general manager North America and Asia, Forbo Flooring Systems, linoleum’s growth was driven primarily by the education segment. He also explained that linoleum’s stable pricing resulted in almost an exact percent of increase for both revenue and volume.

Imports vs. domestic

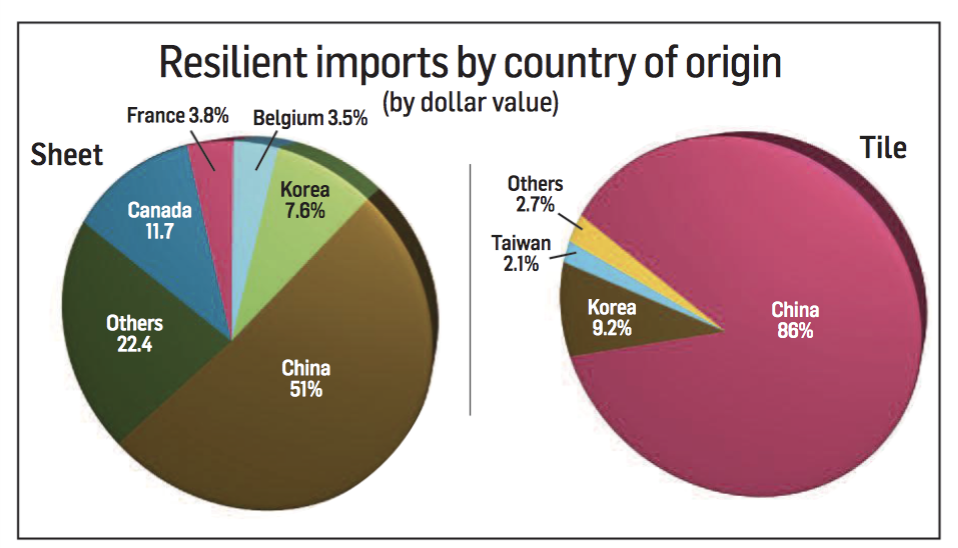

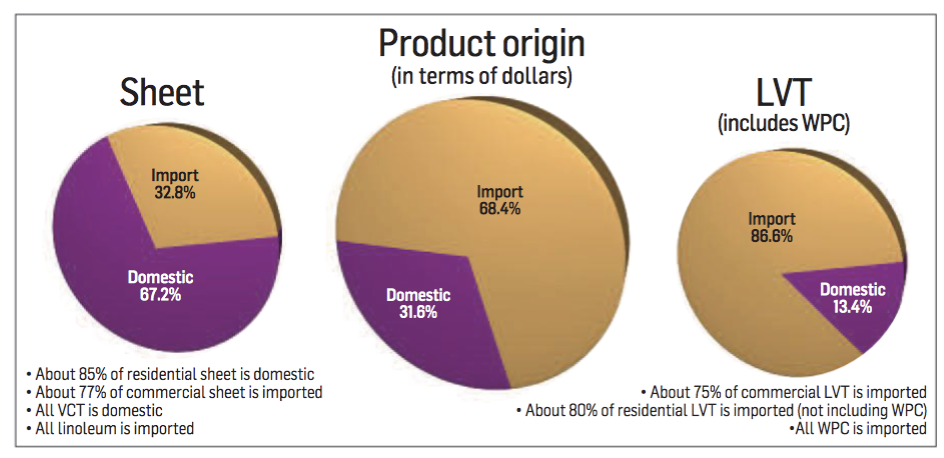

The resilient category is still heavily reliant on import activity with 68.4% of product coming from outside the United States, FCNews research shows. Despite this percentage, domestic production continues to increase, taking a small percentage away from imports. In 2017, domestic production accounted for 31.6% of the category, a slight increase from 2016’s 30.2%.

“There has been a shift toward U.S.-made LVT,” Armstrong’s Block said. He cited the company’s own state-of-the- art facility in Lancaster, Pa., as well as capital investments in its Stillwater,

Okla., facility. “We have invested millions of dollars in the domestic production of LVT to produce resilient flooring in a cost-effective manner, improve styling and be more responsive in servicing key market segments. We’ll continue to balance domestic production and sourcing product to best meet our customers’ needs.”

When looking at specific products, anecdotal research shows approximately 85% of residential sheet is domestic and about 77% of commercial sheet is imported. VCT continues to be virtually domestic, while all linoleum is imported. In terms of LVT, about 75% of commercial LVT is imported. Roughly 80% of residential LVT is made abroad, as is all WPC.

Even though U.S. manufacturers continue to increase domestic production capacities, the bulk of LVT remains imported. According to Beauflor USA’s Finelli, the need for imported LVT products has caused an oversaturation of the market. “You have a lot of overcapacity from import manufacturers that saw a big opportunity in the growth of the LVT category. It’s such a fast-moving product for us that we rely still on our European manufacturing for our LVT. The goal would be to bring that here to the U.S. in the next year or two.”

With both domestic production and imports, the resilient category faces a pricing war. For manufacturers, such as Raskin Industries, newer products have to rely less on beating prices and more on innovative design and proper distribution.

“It can’t be all about price,” Raskin explained. “You need to give on certain products to compete with the large, high-volume, carpet-manufacturing companies and good distributor partners to understand how to work with brands on better items. You need to offer unique designs to separate yourself from the price war.”