Chicago—The forecast for the new home construction market looks cloudy while non-residential sales are expected to remain robust in 2023. Evidence of disinflation—a slowdown in the rapid rise in the rate of inflation—has begun to emerge (building material inflation in particular is easing). However, the full ramifications of the rate of declining prices are not expected to be fully realized in the new year. The irksome supply chain issues that plagued the industry since the onset of the novel coronavirus pandemic have begun to abate—but some challenges still remain as market conditions move slowly toward normalization. And despite the uncertainty and looming threats, U.S. consumers are still poised to continuing spending, albeit at a slightly slower pace.

These competing and seemingly divergent scenarios are indicative of the complex nature of economic forecasting in a time of unprecedented challenges and change for not only the flooring industry but the U.S. economy at large. ITR Economics, which boasts a 94.7% forecasting accuracy rate, is looking to make sense of all this in its critical analysis of the various bellwether market indicators utilized in its forecasts and economic predications. During the 2022 North American Association of Floor Covering Distributors/North American Building Material Distribution Association (NAFCD+NBMDA) convention here this past November, Alan Beaulieu, ITR Economics president, and Connor Lokar, senior forecaster with the firm, shared their outlook for the industry and the U.S. economy for 2023 and beyond.

Following are key points from their respective presentations:

Coping with inflation

The Federal Reserve Board will typically raise interest rates to at least match the consumer price index (CPI), but it appears those rates will pass or overshoot the CPI, according to ITR data. “That’s telling us the Fed seems to be really serious about continuing to raise interest rates, and if they continue to raise interest rates the way they have been, they could easily bring about a recession,” Beaulieu said. “They just want to raise rates—unnecessarily, in our opinion.”

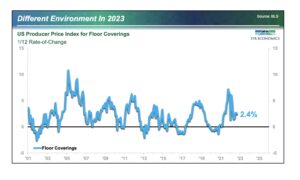

ITR Economics predicts inflation will come down to about 2%-3% by the end of 2023. This amid signs that the rate of inflation, or so-called “disinflation,” is already slowing down. “As inflation comes down to 2%-3% the Federal Reserve Board can claim a win, and it’s happening anyway even without them,” Beaulieu said. “Oil prices were even showing us that, copper prices were showing us that and global PMI was showing us that. There are all kinds of indications that disinflation is going to occur anyway but the Fed can claim the win. And then inflation’s going to come back, it will ebb again down the road in a couple years, then it’s going to come back and it’s going to be a pattern of inflation basically through the rest of the decade.”

As the global economy heals, scarcity of good will become apparent once again, especially for commodities, ITR noted. “And as commodity scarcity comes back, prices will bounce back from where they are today, and as they begin to move up again that creates more inflationary pressures on top of the labor pressures,” Beaulieu noted.

The thing to remember, ITR stressed, is inflation is not horrible—it’s just something everyone has to adjust to. “People will get married, have children, send their kids to college—do all kinds of normal things during a period of inflation,” Beaulieu stated. “You’ll just need to run your business differently.”

Impact on consumer spending

Despite record-high inflation, people will still buy products and spend on home improvements—even if the price of gasoline doesn’t come down as quickly as it went up. “It’s an emotional issue,” Beaulieu stated. “My wife calls me to complain about gasoline prices when I know darn well it won’t change a thing. She’s not going to do less shopping. Nothing is going to change. We get irritated when we have to pay a lot, but that’s all that it is—irritating.

“The reality is consumers are in great shape and businesses are in great shape, and you’re going to find that the economy’s going to continue to move forward. The U.S. economy is not collapsing, despite what you’ve heard from Warren Buffett, Jamie Dimon, George Soros or Newsweek magazine. So, when you read an article online that says, ‘Well, consumers are not spending. It’s because of inflation and consumers are hurt,’ I want you to understand we are at record high levels of consumer spending on an inflation-adjusted basis. Now, there is a segment of the population that’s feeling some pain; I’m not blind to that. But that’s the lower quintile—and the lower quintile doesn’t really represent your target marketplace.”

Another encouraging indicator is the low rate of delinquencies in the U.S. “This is nothing like 2005, ’06 and ’07,” Beaulieu said. “We are in a great position. Businesses, non-financial record high profits. How can you not like that? The only danger is the Fed could do some quantitative tightening, which is not going to help anything as we go forward.”

Commercial prospects rise

During his talk, “Economic Trends in the Construction and Industrial Markets,” Lokar provided an encouraging outlook for the commercial construction industry despite the impact that record-high inflation has had on the residential building market and the U.S. economy overall.

“The macroeconomy is going to be slower in 2023 as we are on the backside of the business cycle—things are slowing down. However, the good news is we’re on fire on the commercial side. We are cruising back toward normal.”

Lokar presented data showing virtually all nonresidential segments are in a recovery or growth mode—led by institutional, lodging, manufacturing and commercial. Moreover, the value of non-residential construction put in place as well as the Architectural Billings Index—key barometers of spending on commercial projects—are in positive territory. Lastly, the multi-family segment of the market (a sector many place in the commercial category) is showing signs of strengthening.

“If the housing market is the locomotive, then the commercial market is the caboose,” Lokar explained. Commercial usually lags GDP by 12 to 16 months. What this means is you can look for some solid commercial market activity in 2023.”

Residential construction dips

Research conducted by ITR Economics shows new home sales are down 18.2% from this time last year. Other warning signs are evident in the rate of sales transactions at Home Depot (down 3% over fourth quarter), although the volume decline is masked by slightly higher prices. Even more telling is the slowing of the rate of home price increases in previously overcooked markets such as Florida and Texas.

“COVID-19 caused consumer behavorial changes, which for housing was euphoric,” Lokar explained. “Now we’re back on trend where we otherwise would have been had we had a normal 2020-2021—at least on the residential side. The housing market is not likely to recover until the second half of 2023.”

Bet big on team USA

The trend toward reshoring—defined by the return of manufacturing jobs to the U.S. that were once outsourced overseas—is real. Whether it’s carpet, furniture or apparel, manufacturing is coming back to America. As the cost of doing business around the world rises, along with the wages and lifestyle of workers overseas—stateside suppliers are recalculating the true cost of manufacturing overseas. In many cases, the numbers support the logic of producing more goods at home—closer to the market that consumes those goods.

At the same time, foreign countries are putting more money and resources into the U.S. market through direct investment. And according to ITR Economics, it’s not who you might think it is. “Most Americans think China is buying the United States, but if you look closely into where foreign direct investment is coming into the United States, Netherlands is the leader,” Beaulieu said. China is No. 13. Luxembourg beats them.

“That tells me the smart money around the world is betting on the United States, and as U.S. businesses, you might want to consider doing the same thing. That’s true for North America in general. Mexico lost a lot of business in China during those globalization years, and some of that’s coming back to Mexico.”

Exports outpace imports

Data supplied by ITR Economics supports a move away from rapid globalization as more factories are built closer to the consuming markets. This trend is partially due to the frailties exposed by the pandemic’s impact on global supply chains. “It’s our thesis—and it’s happening, it’s not just a theory—that we’re going to see less globalization in the years to come,” Beaulieu stated. “We’re going to see more instability in the world, and it’s going to be less reliant upon an elongated supply chain.”

In fact, the U.S. is already seeing imports in key end-use categories decline. “There’s less carpet coming from China, and when we look at vinyl imports from China, it’s slowing down on a year-over-year basis as well,” Beaulieu said. “At the same time, when we look at the European export volume, it’s up and it is increasing—which is good news because that really will help Europe through the winter. However, if you’re sourcing from Europe, that’s going to be a problem. Imports of plywood and veneer wood products are in decline. So, domestically, we have some good things going on, which leads us to the reshoring initiative.”

Return to normalcy

The stimulus-driven ascent the U.S. economy witnessed throughout the first 18 months of the COVID-19 pandemic is dissipating, according to ITR Economics. The hypermarket activity the industry witnessed over the course of the pandemic, though brisk, was not expected to be sustainable over the long term. What all this means for floor covering distributors, retailers, manufacturers and contractors is the industry must adjust accordingly. “If you were reliant on that never-ending growth trend, it’s not going to happen,” Lokar warned. “It’s still trending healthy, but not big growth numbers. The pie is not getting smaller—it just isn’t getting bigger as fast as it did in 2021.”

For the short to medium term, ITR Economics recommends flooring business interests continue to invest in their companies, grow their workforce and keep an eye out for growth opportunities through expansion or acquisitions. “We see materials and component pricing pressure easing, and inflation is getting better—but not tangibly,” Lokar stated. “The market is not going to bring us robust growth in 2023—not through pricing or new business. You are going to have to go get it!”

What all that means, he noted, is the runaway growth that floor covering retailers and distributors experienced in late 2020, throughout 2021 and in the early part of 2022 is not likely to continue this year. Rather, the growth the industry will experience mirrors growth rates seen in non-pandemic years.

Outlook for remainder of 2023

While the market is expected to undergo corrections based on the response to the Fed’s ongoing rate hikes, ITR Economics does expect to see more stability in the near future. “The second half of 2023 is going to be strong, and 2024 is going to be even stronger,” Beaulieu said. “And when this economy of ours gets beyond COVID-19, we are going to go back to business. We are the world’s largest economy and combined with our friends in Canada and Mexico, the North American economy can’t be beat.”

In fact, ITR said it expects the U.S. economy to cruise for at least the next eight years. “This nation and the world is heading toward a great depression around the year 2030,” Beaulieu stated. “The long-term study ITR Economics conducted shows that the United States is going to be the world’s strongest economy through the year 2050. The reality is consumers are in great shape and businesses are in great shape, and we’re going to find that the economy’s going to continue to move forward, which will have a positive impact on your businesses.”